Week Six: Luddite Ventures

My life motto should be, "fast to try, slow to be convinced."

Housekeeping

Welcome to the sixth edition of Venture Vantage. We’ll be exploring topics related to tech and the venture ecosystem.

I would like to take a moment of silence to commemorate the late Summer 2024. She is officially dead, and I am grieving. Shiva will be held at the Canada Goose store in SoHo.

As always, please hit me back with feedback and comments—I’m constantly seeking ways to make this newsletter a more valuable read.

Diving right in and keeping things brief:

The Meat & Potatoes

A post-mortem: Bird scooters

Context:

Bird was founded in 2017 by Travis VanderZanden. The company was started in Santa Monica.

Travis was ex-Lyft and ex-Uber prior to starting Bird.

The initial goal of Bird was to provide mass-consumer last-mile transit, helping people get from public transportation stops to their final destination.

Bird launched in Santa Monica in September of 2017. Santa Monica was a prime candidate for Bird: good weather, not too hilly, a tight-knit public transit network, and very bike-friendly.

Bird operated on an “ask for forgiveness, not permission” strategy, never formally seeking approval from the City of Santa Monica prior to their launch. Bird would quietly distribute scooters overnight, often catching city residents and officials off-guard.

After Bird had gained some traction, they began lobbying for regulatory approval. Bird spent a lot of money lobbying to get regulation like CA AB 2989 passed.

Bird tried to build a moat with a network effect—they figured that by being the dominant company (having the most scooters), consumers would prefer them. The thought process was that once a user had the Bird app downloaded, the likelihood that they would sign up for a competitive service would drop drastically.

Bird introduced a gig economy model for recharging and maintaining scooters, known as “Chargers.” Anyone could sign up to collect scooters that needed recharging, charge them overnight, and return them to designated areas in the morning. This model allowed Bird to scale quickly without needing a large in-house operations team.

Bird attributed a lot of its success to their referral program, which rewarded users for referring friends. The experience of taking a Bird scooter was also often a social activity, in which friends would get from point A to point B together by taking a Bird scooter.

In October 2018, Bird launched Bird Zero, their first in-house electric scooter. That same year, they raised a $300M Series C from Sequoia, making the company a unicorn.

The following year, they raised another $275 million in a Series D, led by CDPQ and Sequoia.

Bird hired hundreds of employees to manage and oversee their fleets. Many of these fleet managers were judged and scored based on a variety of metrics, from how many scooters were stolen to how many were knocked over on the side of the road.

In September 2023, Bird acquired their competitor, Spin, for $19M.

Spin was originally backed by Ford, with their desire to have a foot in the micro-mobility space.

Bird’s operating expenses were through the roof. Unfortunately, they had a high cost of repair associated with a trend called “Bird droppings,” where people would throw the scooters off of buildings, and destroy them for fun.

Bird’s burn rate after acquiring Spin was as high as $30M/month.

Data suggested that each scooter had an average lifespan of about 28 days.

For the scooters that made it past that, they cost up to $200/month in maintenance.

Charging costs were up to $20/charge/scooter.

At their peak, Bird had upwards of 1,000 employees.

In the early stages of COVID, Bird laid off 30% of its workforce almost immediately. COVID was fairly detrimental to Bird's revenue, but its revenues would not have been enough to keep the company afloat.

Bird went public via SPAC in November 2021, and performance was poor almost right off the bat.

In November 2022, Bird disclosed that it had overstated revenue by recognizing unpaid customer ride balances as revenue. This majorly impacted stock prices and how investors perceived Bird.

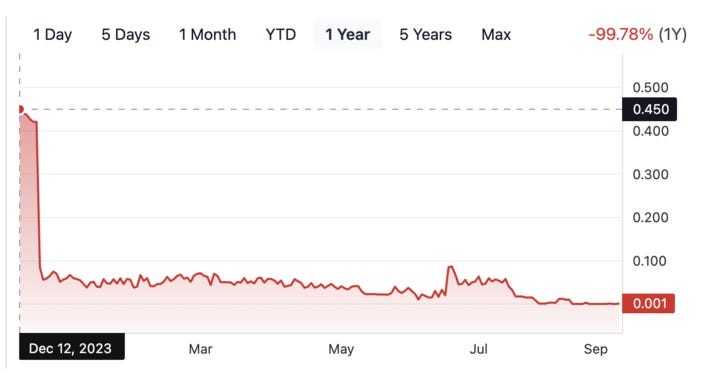

In December of 2023, Bird filed for bankruptcy. Once sitting at a $2.5B valuation, the company was now worth nothing.

As of April of this year, Bird has emerged from Chapter 11 bankruptcy.

As of today, Bird Scooters are owned by Third Lane Mobility Inc.

Bird successfully emerged from Chapter 11 bankruptcy in early 2024, and Third Lane Mobility, a newly organized private parent company, acquired its assets. Third Lane Mobility now operates Bird and Spin brands.

Vantage:

Bird’s death is a great example that pre-mature celebration can be an achilles heel in the world of venture. You truly never know when a company is going to tank—it can be after you’ve already chalked it up as a success.

We saw a few funds tout Bird as the darling of their portfolio. We now understand today why that can be such a dangerous, and bad thing.

Besides being a premature celebration, it also creates bitter feelings within the portfolio. Imagine being one of the portco founders who was still successful and gave a great return to the fund (maybe even better than Bird), but who didn’t receive the same parade that Bird received.

I consider it to be a premature celebration because a fund manager has to (simplified) do four things really well: 1) source 2) select 3) support and 4) sell. Leaving DPI on the table, which a lot of these funds did out of poor timing, leaves you as a bad fund manager in the fourth category.

Bird is a great case study for why flooring the gas on a direction-less car is a terrible, terrible idea. Ensuring that there is good and constantly iterated upon strategy is essential to the long-term success of the business.

If something is not fundamentally a good business on day one, it will never be a good business. While companies can benefit from economies of scale, a solid business model cannot be understated, even though it often is in the world of venture.

News, Deals, and Pretty Things

Perplexity is going after the big bucks

Context:

Perplexity is trying to raise a $500M at an $8B valuation.

This is Perplexity’s third round of fundraising this year.

In January, they raised at a $520M valuation.

Over the summer, they raised at a $3B valuation.

Today, they’re over 10x from where they were 10 months ago. That’s fairly unprecedented for this late stage of growth venture funding.

As a comp, OpenAI just raised $6.6 billion in its last round at a valuation of $157 billion. These AI valuations are off the charts, especially considering very few of them are generating substantive or reliable revenue.

Vantage:

Valuation climbs like these are, in my opinion, entirely unsustainable. There is no healthy revenue multiple to be basing these valuations on, so investors end up bidding an asinine amount of money on companies that have no real chance of ever returning DPI.

I wonder how much of it is a vicious cycle in which funds are pushing other funds to invest, despite it being a bad idea, to inflate their own TVPI.

What is the liquidity plan for the funds that enter at this $8B valuation? Do they hope to quickly offload their shares in a year or two on the secondary, and pray for a 2x or 3x in valuation? I feel like there are less risky ways to do that.

Freaking finally, Apple.

Context:

Apple is finally getting closer to launching the features they promised in their “It’s Glowtime” event.

In the developer beta of iOS 18.2 that came out today, users can finally test a few new features:

Genmoji

Image Playground

More AI writing features

ChatGPT integration

and Visual Intelligence.

The non-beta version of iOS 18.1 that offers notification summaries and a marginally smarter Siri is slated to go public next week.

Apple is still missing some pretty key features they promised during the keynote, like the ability for Siri to understand and contextualize whatever is on a device’s screen at any given moment.

Apple Intelligence is still not available in the EU or China, two massive markets for Apple.

Vantage:

Apple was likely under a lot of pressure from all angles, consumers, developers, and investors, to launch the features they touted at the September event.

The reviews for the iPhone 16 Pro series have been pretty damning so far—it’s become widely talked about that the new devices don’t have much to offer in the way of innovation, and are nearly identical (from a usage perspective) to the last generation.

I think Apple is largely realizing that they simply don’t have the talent to compete with the big boys in the space, and are having a hard time hiring for it.

Apple is inherently not a company that is designed for AI. It will instead have to pivot to adopt AI, which can be challenging when so much of the staff has little to no experience in either developing or integrating AI products.

Main point here: I was on a work call this morning prior to a strategic planning session with a portco, and we got to talking about AI.

My thesis was this: AI is simply another foundational technology that will be filed on the history shelves as better technologies emerge. It is not destined to be a front-end technology but rather a back-end technology.

The status quo of AI is pretty terrible from a user-centric design perspective, much like web3/blockchain was. The true future is a more seamless communication and integration with our technology, which AI has the potential to do, not be another separate dialogue or chatbot that requires attention in an already crowded UI.

For as long as you can “see or feel the layer of AI,” it won’t have a large impact on the world, and will be largely undifferentiated.

AI will really make a splash when it operates quietly on the backend to make the product better and easier to use, without the user ever having to think about it.

Could I be wrong about this? Absolutely. I’ve always joked that I should start a fund called Luddite Ventures or Skeptic Ventures. I am always fast to try and slow to be convinced about new tech. However, there are far too many qualities of AI that, to me, are eerily similar to blockchain. The biggest of which is people forcing it into products that could very well live without it.

Uber might buy Expedia

Keeping this one short… it’s been a long day, and I’m fading quickly.

Context:

Uber has reportedly been exploring an acquisition/merger of Expedia, the travel platform.

There’s not a lot of information out there, but there are some pretty legit sources confirming it. Expedia was asked for a comment and they said, “We don’t comment on rumours and speculation.”

I thought that was pretty funny.

Expedia spends over $2B a year, according to one source, on SEO. Integrating into Uber could save them on some of those crazy costs.

Vantage:

Uber has been hungry to go after multiple different markets and part of the travel experience, making them a swiss army knife app. They went after micro-mobility with Lime, food delivery with Postmates, logistics with Transplace, they launched a rental car service, and even have done boats and helicopters. Acquiring Expedia would allow them to own a foot in nearly every aspect of the travel planning industry, including flight bookings.

Uber’s CEO, Dara Khosrowshahi, is way too familiar with Expedia: he was the CEO from 2005 to 2017, in which he led some pretty stellar growth. He knows that business inside and out.

Deals that caught my eye

Continuing this trend from last week. I think it’s helpful to just have some kind of pulse of the funding markets.

Windmill Air raised a $5M Series A led by YETI Capital, Pentland Ventures, Dot Capital, SuperAngel.Fund, and other investors.

I have a Windmill AC in my apartment and it rocks, so I totally see them going to the moon.

Compare them to the lightbulb industry mentioned below.

Fixify just raised a $25M Series A. The round was led by Costanoa Ventures, Decibel Partners and Paladin Capital Group.

They do something every similar to what I added in the White Hot section last week: they are a support ticket platform for IT help desks.

They use AI to unlock efficiency in the customer service chain.

Reality Defender just raised $33M in a Series A to combat deep fakes. Investors include Illuminate Financial, Booz Allen Ventures, IBM Ventures, the Jeffries Family Office, Accenture, DCVC, and The Partnership Fund for New York City. '

Passkey Therapeutics raised $20M in their seed round from Breakout Ventures, Innovation Endeavors, Bison Ventures, Wireframe Ventures, Alexandria Venture Investments, and GRIDS Capital.

Freeform raised $14 million from Boeing AE Ventures and Nvidia, in addition to the $45M they’ve already raised. The two new investors in this round will also provide Freeform with other resources, such as graphics cards. The company provides metal 3D printing as a service with a focus on aerospace, automotive, and industrial sectors.

White Hot

Human Health:

Connected gym equipment. As winter sets in, the number of activities posted to Strava tends to drop off fairly drastically, especially in colder-climate regions. Not everyone has access to Zwift or other connected experiences, and instead rely on local gyms. Equipment that enables athletes to track workouts and progress in the gym is of growing importance.

I am certain there will soon be a bone health revolution. We are learning more and more about how much our bones contribute to our overall wellbeing, and diseases like osteoporosis affect more than 16% of the American population. There are huge markets that are desperate for bone care that simply does not exist.

Posture has collapsed in younger generations. As we spend all day sitting in front of digital devices, our posture is visually failing us. Tools are needed to correct this.

Future of Work:

Automation workflows that help teams reduce the number of clicks it takes to get through repeated tasks. For example, onboarding a new employee with just one click: automating payroll setup, email creation, adding them to Slack, etc.

Platforms that allow niche professions a single solution to run their entire businesses. A great example is what Clio has done for law.

Far too many businesses spend large amounts of money on an office manager, only for the office to still be an operational mess. I don’t know what the form factor would be for a solution, but far too many offices are faced with the problem of disorganization, missing supplies, and pure chaos.

Infrastructure:

There are $1.5B worth of light bulbs sold each year in the US. Philips manufactures 25-30% of those light bulbs. The lightbulb industry has nearly no brand loyalty, and is ripe for true disruption.

Modularity of vehicles is around the corner. As EVs step into the spotlight and the right-to-repair movement gains momentum, the average lifespan of cars will increase substantially with modular parts that can easily be hot-swapped for newer parts.

Improved solutions for electrical engineering that reduce the need for manual planning, as well as laborious custom installation solutions. 5-10% of the total construction budget of a new single-family dwelling goes towards electrical.

Some cool stuff on my radar

The coolest thing I’ve seen this week is the Saga bike. This goes directly back to my first point in the White Hot section.

One of my favorite things that I own is the Rolling Square AirCard.

Backstory: I lost my wallet for 18 hours a few years ago, and slowly descended into madness over those 18 hours. I retraced every step, ripped apart my entire frat house bedroom, and searched every classroom, only to find my wallet hidden in my backpack. When I found my wallet, I had already canceled every single card. I swore I would never do that again, and bought a Tile tracker, but it quite frankly sucked. I discovered the AirCard when they were on Kickstarter, and picked it up. I was recently reminded of it (yesterday) because I couldn’t find my wallet on me. As I slowly descended into madness over the course of 60 seconds, I remembered I had the AirCard. I immediately returned to my happy, regular day without the stress of a lost/misplaced wallet.

The AirCard’s battery lasts forever. I’ve had it for a while, and it has never needed a battery replacement, when my traditional AirTags have needed about 2 replacements in the same period of time.

I did so much research around the best winter shoes for NYC, and these Blundstones are the ones that kept coming up. They’re waterproof, slip-on, and supposedly really comfortable. I just bought a pair, and they’re worth checking out if you’re looking for a new pair, too.

Closing

Thanks for taking time out of your Wednesday to read. Enjoy the freezing cold weather while I figure out how to get myself onto a tropical island.

As always, you can find me on X and LinkedIn, and I’d love to hear from you via email. Whether it’s talking startups or just shooting the shit, I’m always happy to connect.

Onto the next!

//Eli